Pay-Per-Call for Insurance: Auto, Health, Medicare & Final Expense (2026)

Pay per call insurance leads explained for 2026: how inbound insurance calls work across auto, health, Medicare, and final expense, plus payouts, call quality filters, TCPA compliance, and routing setup.

Rafael Hernandez

Founder & CEO

Ex-Microsoft SWE · $10M+ PPL ad spend

I hope you enjoy reading this blog post. If you want to try Lead Distro AI for free, click here.

Author: Rafael Hernandez | Founder & CEO of Lead Distro AI

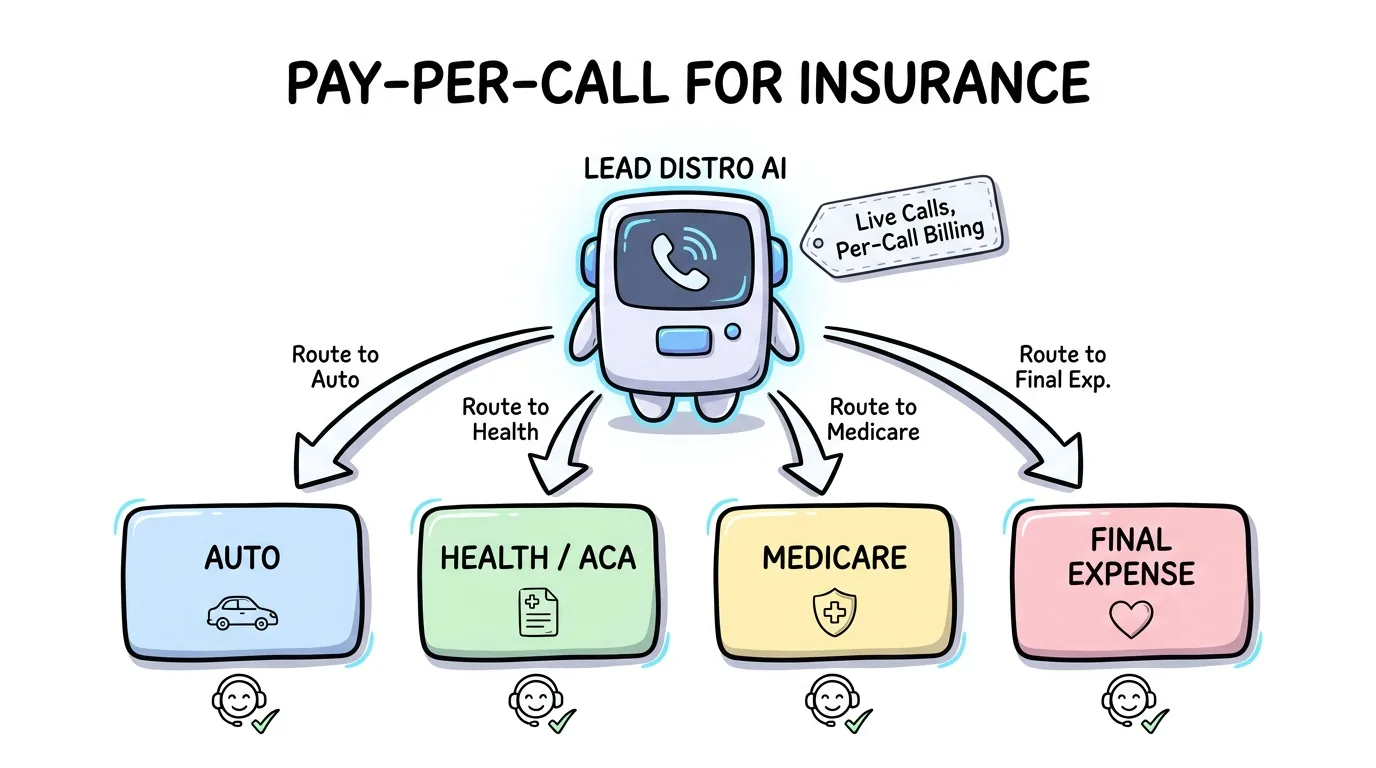

Pay per call insurance leads are inbound phone calls from consumers shopping for an insurance policy, sold to a licensed agent or call center on a per-call basis rather than per form fill. A publisher generates the call through search ads, SEO, or a quote site, a tracking number routes the live caller to a buyer, and the buyer pays an agreed price once the call passes a duration or qualification threshold. For insurance agencies, this model converts faster than data leads because the prospect is already on the phone with intent. For pay-per-call agencies, insurance is one of the highest-payout verticals available, spanning auto, health and ACA, Medicare, and final expense.

This guide breaks down how pay per call works for insurance, what each major insurance call category is worth, how to filter for call quality, the TCPA compliance rules that govern outbound and inbound insurance calls, and how to set up routing, billing, and tracking with Lead Distro AI. It closes with an honest comparison of pay-per-call against shared and exclusive insurance leads so you can decide which model fits your operation. If you run both calls and data leads, see how one platform handles both in the product tour.

Key Takeaways

- Pay per call insurance leads are billed per qualified call, not per form fill, which shifts risk toward call quality and away from contact-rate guesswork that plagues shared data leads.

- The four core insurance call categories are auto, health/ACA, Medicare, and final expense, and each carries a different payout, seasonality (Medicare AEP, ACA open enrollment), and buyer-filter profile.

- Call quality is enforced with buyer filters: minimum call duration, IVR pre-qualification, state and license matching, and duplicate suppression decide whether a call bills.

- TCPA governs insurance calls: the law requires prior express written consent for autodialed or prerecorded telemarketing, and the FCC's one-to-one consent rule was vacated by the courts in January 2025, so document consent and scrub Do-Not-Call lists rather than relying on a single registry rule.

- Routing, billing, and tracking run on a distribution platform using Round Robin, Weighted, Priority/Waterfall, or Ping-Post, with usage-based call tracking layered on the flat subscription.

- Pay per call beats shared insurance leads on speed-to-contact but exclusive data leads still win for agencies that want to own the prospect record and nurture over time.

How Pay-Per-Call Works for Insurance

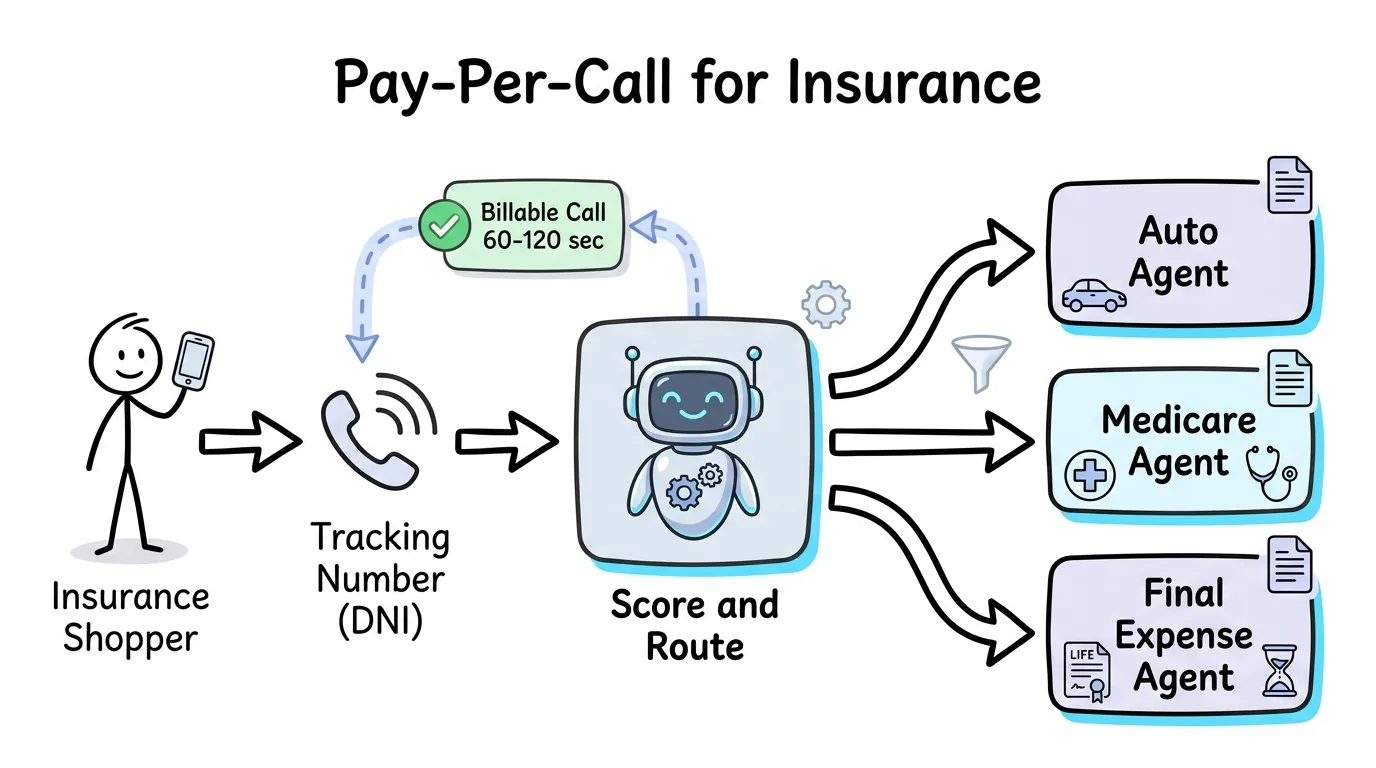

Pay per call inserts a tracked phone number between a publisher and a buyer. The publisher runs an insurance campaign (a Google search ad for "Medicare plans near me," an ACA quote landing page, an auto insurance comparison site) and displays a tracking number. When a consumer calls, the platform's Dynamic Number Insertion (DNI) ties that call to its source, scores it, and routes the live caller to a buyer based on rules the buyer set: vertical, state, time of day, and bid.

The buyer only pays when the call clears a threshold, usually a minimum connected duration (commonly 60 to 120 seconds) plus any IVR pre-qualification answers. That billable event protects buyers from junk calls and pushes publishers to send genuinely interested callers. The result is a marketplace where insurance agencies buy live intent at a known unit cost, and pay-per-call agencies monetize call inventory across multiple buyers without managing the policy sale themselves.

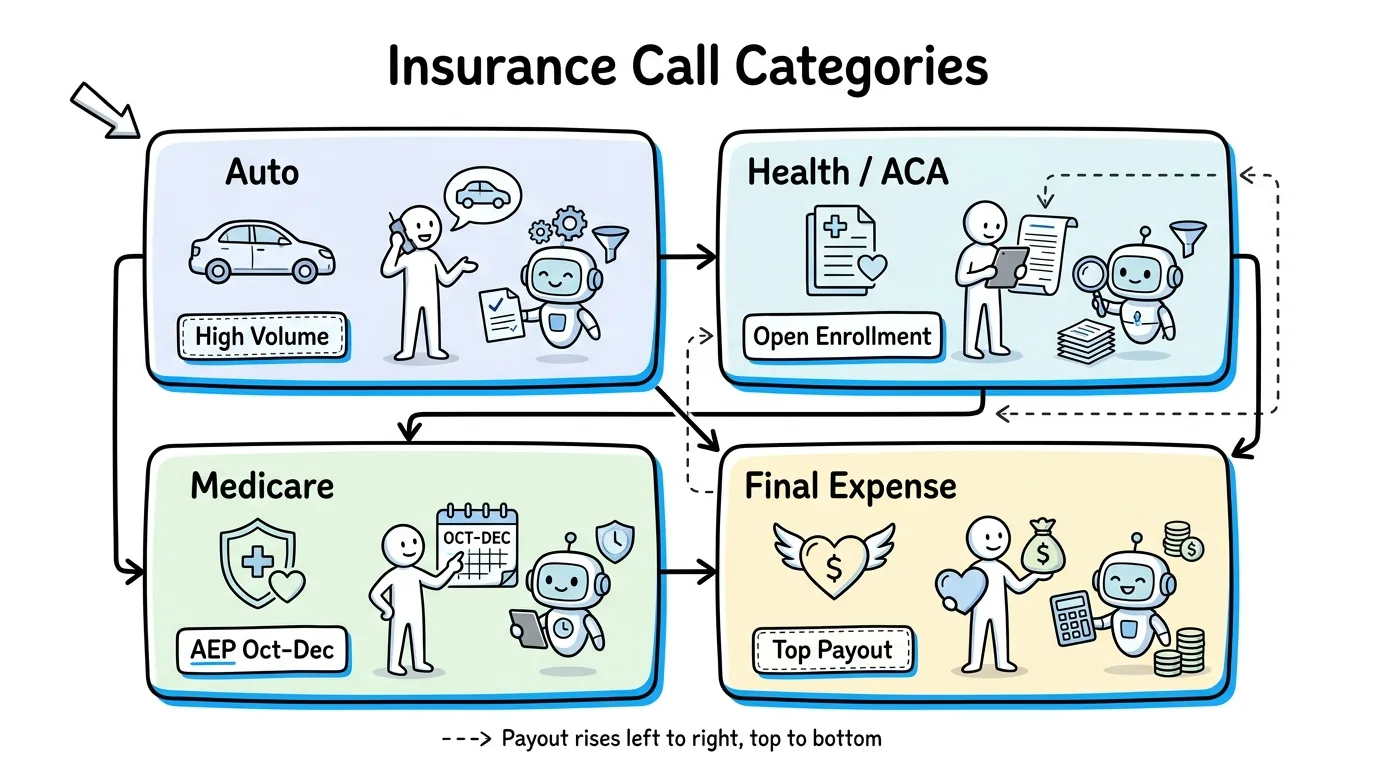

The Four Core Insurance Call Categories

Insurance pay-per-call inventory splits into four buyer-defined categories. Each behaves differently on payout, seasonality, and the filters buyers apply before a call bills.

Auto Insurance

Auto is the highest-volume insurance call vertical because demand is year-round and intent is concrete (a new car, a rate hike, a lapsed policy). Calls are filtered on state, current coverage status, and sometimes the presence of a recent accident or DUI. Auto calls tend to sit at the lower end of insurance payouts per call because volume is high and the policy value per sale is modest relative to life lines.

Health and ACA

Health and Affordable Care Act (ACA) calls spike during the federal open enrollment window, typically November 1 through mid-January, set by the Centers for Medicare and Medicaid Services. Buyers filter heavily on subsidy eligibility, household income band, and state of residence. These calls carry strict compliance exposure because ACA marketing rules and CMS oversight apply on top of the TCPA.

Medicare

Medicare calls (Medicare Advantage and Medicare Supplement) peak during the Annual Enrollment Period (AEP), which runs October 15 to December 7 each year (Medicare.gov, Joining a plan). Buyers filter on age 65-plus, current plan status, and county, since Medicare Advantage plans are county-specific. Medicare is among the highest-payout insurance call categories, and CMS marketing rules require additional disclosures and call recording, so compliance discipline is non-negotiable.

Final Expense

Final expense (small whole-life policies covering burial costs) targets an older demographic, usually 50 to 85. Calls are filtered on age band and state. Final expense often commands strong per-call payouts because the policies are simple to close and recurring premium is predictable. Buyers prize call quality here because the demographic responds poorly to repeated contact, making first-call connection critical.

Insurance Call Types by Intent and Typical Payout

The table below summarizes how the four categories compare on buyer intent, seasonality, and where each tends to fall on the payout scale. Exact payouts vary by buyer, state, and call quality, so treat these as relative positioning, not fixed prices.

| Insurance Call Type | Buyer Intent | Peak Season | Typical Payout Tier | Primary Buyer Filters |

|---|---|---|---|---|

| Auto Insurance | High, switch or new policy | Year-round | Lower | State, coverage status, driving record |

| Health / ACA | High, subsidy and plan shopping | Nov to mid-Jan (OEP) | Mid | Income band, subsidy eligibility, state |

| Medicare | High, plan selection at age 65+ | Oct 15 to Dec 7 (AEP) | Higher | Age 65+, county, current plan |

| Final Expense | Moderate to high, coverage gap | Year-round | Higher | Age 50-85, state |

The pattern that matters: payout follows policy value and lifetime premium, not call volume. Auto sends the most calls but pays the least per call; Medicare and final expense send fewer calls but command higher payouts because each closed policy is worth more to the buyer over time. A pay-per-call agency building an insurance portfolio usually anchors on Medicare and final expense for margin, then layers auto for volume and cash flow between enrollment seasons.

Call Quality and Buyer Filters

In pay per call, quality is not a vibe, it is a set of enforced rules that decide whether a call bills. The most common filters insurance buyers apply are:

- Minimum call duration. A call must stay connected for a set time (often 60 to 120 seconds) before it counts as billable. This screens out hang-ups and accidental dials.

- IVR pre-qualification. An interactive voice response menu asks one or two questions (age, state, current coverage) before transfer, so only callers who match the buyer's criteria connect.

- State and license matching. Insurance is regulated state by state, so calls route only to agents licensed in the caller's state. Sending an out-of-state call wastes the buyer's spend and creates compliance risk.

- Duplicate suppression. The same caller within a defined window is blocked from billing twice, protecting buyers from being charged for repeat dials.

- Concurrency and cap controls. Daily and hourly caps prevent a buyer from being flooded beyond what their agents can answer live.

An original insight from running mixed call-and-lead operations: the single biggest driver of insurance pay-per-call profitability is not the payout, it is the gap between gross calls and billable calls. Two publishers quoting the same per-call price can deliver wildly different net economics once duration thresholds, duplicate suppression, and state mismatches are applied. Buyers who measure billable-rate by publisher, not just volume, consistently pay less for better calls. That is why scoring and filtering before routing, rather than after billing, is the lever that protects margin.

TCPA and Compliance for Insurance Calls

Insurance is one of the most heavily regulated pay-per-call verticals, so compliance is a buying decision, not an afterthought. The governing federal law is the Telephone Consumer Protection Act (TCPA).

The TCPA requires prior express written consent before making autodialed or prerecorded or artificial-voice telemarketing calls and texts to consumers, and it restricts calls to numbers on the National Do-Not-Call Registry (FCC, Telemarketing and Robocalls). Statutory damages run from $500 to $1,500 per violating call or text under the statute, which is why documented consent is the foundation of any compliant insurance call program.

One development is widely misreported, so state it accurately: the FCC's 2023 "one-to-one consent" rule, which would have required separate consent for each individual seller, was vacated by the U.S. Court of Appeals for the Eleventh Circuit in Insurance Marketing Coalition Ltd. v. FCC on January 24, 2025, before it took effect (Eleventh Circuit decision coverage, Kelley Drye). The pre-existing prior-express-written-consent standard remains in force. Do not market a "one-to-one consent required" rule as current law.

Practical compliance steps for insurance pay-per-call:

- Capture and retain consent records for every lead source: timestamp, IP address, the exact consent language, and the form URL.

- Scrub against the National Do-Not-Call Registry and any internal opt-out list before outbound contact.

- Record calls where required (Medicare and ACA marketing carry CMS recording and disclosure obligations on top of the TCPA).

- Match callers to state-licensed agents so no agent solicits in a state where they are unlicensed.

"Consent documentation is the single most decisive factor in TCPA litigation. Companies that retain granular, per-lead consent records resolve claims far faster than those relying on blanket attestations," says Eric Troutman, founder of TCPAWorld and a nationally recognized TCPA defense attorney.

This is general information, not legal advice. Confirm current requirements with qualified counsel before launching insurance calling campaigns.

Routing, Billing, and Tracking With Lead Distro AI

Once calls are flowing, the platform layer decides who gets each call, how it bills, and how it is tracked. Lead Distro AI handles insurance pay-per-call with four distribution methods:

- Round Robin spreads calls evenly across a buyer pool so no single agent is starved or flooded.

- Weighted sends a higher share of calls to your best-performing or highest-paying buyers.

- Priority/Waterfall offers each call to the top buyer first and falls down the list if they decline or are capped (the same model often called a waterfall).

- Ping-Post broadcasts the call's qualifying attributes to multiple buyers in real time, collects bids, and routes the live caller to the highest bidder, the revenue-maximizing model for high-payout lines like Medicare.

Every inbound call is scored with AI before routing, so buyers receive pre-qualified callers rather than raw inbound volume. Tracking runs on Dynamic Number Insertion, attributing each call to its publisher and campaign. Billing is reconciled per buyer in real time with P&L by source.

On pricing: the platform subscription starts at $299 per month flat. Call tracking is billed separately and is usage-based, a per-tracking-number monthly fee plus a per-minute rate for inbound calls, layered on top of the subscription. A 7-day free trial is available with a credit card required. To see routing, scoring, and ping-post bidding in an insurance workflow, start your free trial or read the insurance vertical overview. For deeper tooling comparisons, see our best ping-post software for insurance and best pay-per-call software for agencies guides. For other call verticals and the agency tooling behind them, see pay-per-call for home services and call tracking for agencies.

Pay-Per-Call vs Shared and Exclusive Insurance Leads

Pay per call is one of three ways to buy insurance demand. Each fits a different operation.

Pay per call delivers live, phone-ready prospects and bills per qualified call. Speed-to-contact is instant because the prospect is already on the line, which is its biggest advantage over data leads where contact rates can be low. The trade-off is less control over the prospect record and higher per-unit cost.

Shared data leads are form fills sold to several buyers at once, cheap per lead but contact rates suffer because the prospect is fielding multiple calls. They suit high-volume operations that can dial fast and win on speed.

Exclusive data leads are sold to one buyer, carry a higher cost per lead, and let an agency own the prospect record and nurture over time. They suit agencies that want a CRM-driven, long-cycle sales motion. For the full breakdown of buying and routing form leads, read our insurance lead generation guide and the best lead distribution software for insurance agencies. For line-specific demand, see our health insurance lead generation and Medicare leads guides.

The strongest insurance operations do not pick one. They run pay per call for high-intent enrollment-season volume and exclusive data leads for year-round nurture, distributing both from a single platform so the P&L is unified.

FAQ

What are pay per call insurance leads?

Pay per call insurance leads are inbound phone calls from consumers shopping for an insurance policy, sold to a licensed agent or call center on a per-qualified-call basis rather than per form fill. A publisher generates the call through ads, SEO, or a quote site, a tracking number routes the live caller to a buyer, and the buyer pays once the call clears a duration or pre-qualification threshold. The model favors speed-to-contact because the prospect is already on the phone with active intent.

Which insurance call types pay the most?

Payout follows policy value and lifetime premium, not call volume. Medicare and final expense calls typically command the highest per-call payouts because each closed policy is worth more to the buyer over time. Auto insurance sends the highest call volume but pays less per call. Health and ACA calls sit in the middle and concentrate around the open enrollment window. Exact payouts vary by buyer, state, and call quality, so a pay-per-call agency usually anchors margin on Medicare and final expense, then layers auto for volume.

Is pay per call insurance TCPA compliant?

Pay per call can be fully TCPA compliant when consent and Do-Not-Call rules are followed. The TCPA requires prior express written consent for autodialed or prerecorded telemarketing calls and texts and restricts calls to numbers on the National Do-Not-Call Registry. The FCC's 2023 one-to-one consent rule was vacated by the Eleventh Circuit in January 2025 and never took effect, so the prior written-consent standard governs. Retain per-lead consent records, scrub DNC lists, and record calls where Medicare or ACA rules require it. This is general information, not legal advice.

How is call quality enforced in pay per call?

Call quality is enforced with buyer filters applied before a call bills: a minimum connected duration (often 60 to 120 seconds), IVR pre-qualification questions, state and license matching, duplicate suppression, and daily or hourly caps. These rules decide whether a call counts as billable, which protects buyers from junk inventory and pushes publishers to send genuinely interested callers. Measuring billable-rate by publisher, not raw volume, is the clearest way to control insurance pay-per-call margin.

How do I route and bill insurance calls?

Insurance calls are routed and billed on a distribution platform. Lead Distro AI supports Round Robin, Weighted, Priority/Waterfall, and Ping-Post distribution, scores each call with AI before routing, and attributes calls with Dynamic Number Insertion. The platform subscription starts at $299 per month flat, and call tracking is usage-based on top of that, a per-number monthly fee plus a per-minute inbound rate. A 7-day free trial is available with a credit card required.

What is the difference between pay per call and shared insurance leads?

Pay per call delivers live, phone-ready prospects and bills per qualified call, so speed-to-contact is instant. Shared data leads are form fills sold to several buyers at once, cheaper per lead but with lower contact rates because the prospect fields multiple calls. Pay per call wins on intent and immediacy; shared leads win on raw cost and suit high-volume dialing operations. Many agencies run both, plus exclusive leads for long-cycle nurture, from one platform.

Conclusion

Pay per call is the fastest path to live insurance intent, and across auto, health and ACA, Medicare, and final expense it gives agencies a per-call cost they can model and pay-per-call operators a high-payout vertical to build on. The economics turn on call quality and compliance: enforce buyer filters before routing, document consent under the current TCPA standard, and route with the method that fits each line, with Ping-Post earning the most on high-payout Medicare and final expense calls.

If you want to run insurance calls and data leads from one dashboard with AI scoring and real-time P&L, start your free 7-day trial and route your first call in under an hour. See the insurance vertical page for the full feature set, or take the product tour to watch ping-post bidding work end to end.

Building an insurance pay-per-call book? Start your 7-day free trial and see how Lead Distro AI scores, routes, and bills auto, Medicare, health, and final expense calls from one platform. Credit card required.

About the Author

Founder & CEO of Lead Distro AI & Great Marketing AI

UC Berkeley graduate and former software engineer at Microsoft. Rafael built Lead Distro AI after managing over $10M in ad spend for performance marketing agencies (pay-per-lead and pay-per-call), including running campaigns for Neil Patel. He combines deep software engineering expertise with hands-on performance marketing experience to build tools that help these agencies scale profitably.

About Lead Distro AI

Lead Distro AI: AI-Powered Lead Distribution & Call Tracking That Maximizes ROI

The modern platform for pay-per-lead and pay-per-call agencies. Route, score, and deliver leads with AI-powered automation and real-time P&L tracking. Built for performance marketing agencies and lead buyers across legal, insurance, mortgage, solar, and home services verticals.

4 Distribution Methods

Waterfall, Round Robin, Weighted, Ping-Post

Ping-Post Auctions

Real-time bidding with sub-second routing

Real-Time P&L Reporting

Track revenue, costs, and profit per campaign

Call Tracking

Assign tracking numbers, record calls, and attribute conversions

AI Lead Scoring

Score every lead before routing to maximize conversion

Partner Portal

Self-serve dashboard for buyers to track leads