Auto Insurance Leads: How to Buy, Price, and Distribute

Buy and sell auto insurance leads in 2026: lead types, CPL benchmarks, exclusive vs shared pricing, real-time ping-post delivery, filters, caps, and TCPA rules.

Rafael Hernandez

Founder & CEO

Ex-Microsoft SWE · $10M+ PPL ad spend

I hope you enjoy reading this blog post. If you want to try Lead Distro AI for free, click here.

Author: Rafael Hernandez | Founder & CEO of Lead Distro AI

Last Updated: June 27, 2026

Auto insurance leads are the contact records of consumers actively shopping for car insurance, sold to carriers, independent agents, captive agents, and aggregators who want to quote and bind new policies. The United States has more than 230 million licensed drivers (Federal Highway Administration), and the average driver pays well over $2,500 a year for full coverage (Bankrate), which makes auto insurance one of the highest-volume, most-shopped lead verticals in pay-per-lead. A shared lead typically sells for $4 to $12, an exclusive lead for $12 to $30, and a live-transfer call for $25 to $55, depending on the state, the driver profile, and how fresh the record is.

Whether you generate leads yourself through Google Ads quote funnels or buy them wholesale to resell, the economics come down to one thing: getting each lead to the right buyer fast, with clean filtering and accurate billing. This guide breaks down the lead types, 2026 pricing benchmarks, real-time delivery and ping-post mechanics, TCPA compliance, and how a platform like Lead Distro AI routes auto insurance leads at scale. Start your free trial and route your first lead in minutes.

Key Takeaways

- Auto insurance leads are a high-volume, mid-priced vertical, with shared records at $4 to $12, exclusives at $12 to $30, and live-transfer calls at $25 to $55 in 2026.

- Lead type drives price more than anything else, in this order: live transfers, exclusive real-time records, shared records, then aged lists sold at a fraction of the original cost.

- Speed to lead decides who wins the policy. Harvard Business Review research found firms that respond within an hour are nearly 7 times more likely to qualify a lead, so real-time delivery matters most in auto.

- Filtering protects margin. State, ZIP code, driver age, SR-22 status, and currently-insured flags should route the lead before it ever reaches a buyer.

- Lead Distro AI distributes auto insurance leads across all four methods (Round Robin, Weighted, Priority/Waterfall, Ping-Post) with AI scoring, real-time P&L, and built-in consent logging.

What Auto Insurance Leads Are and Who Buys Them

Auto insurance leads come from drivers requesting a quote through a comparison site, a landing page, a Facebook lead form, or an inbound call. Each record carries the contact details plus rating signals a buyer needs: ZIP code, vehicle, current carrier, coverage level, and whether the driver is currently insured.

The buyer side is deep. Captive agents from national carriers, independent agents who quote several carriers, large aggregators, and pay-per-lead networks all compete for the same consumer. Auto remains one of the most-shopped personal insurance lines in the country (Insurance Information Institute), which is why it is a reliable resale vertical for lead buyers and lead sellers alike.

Most sellers run a mix: generate some volume in-house, buy the rest wholesale, then redistribute. The margin lives in the spread between what you pay to source a lead and what a buyer pays to receive it, minus duplicates and returns. That is exactly the spread a distribution platform is built to protect.

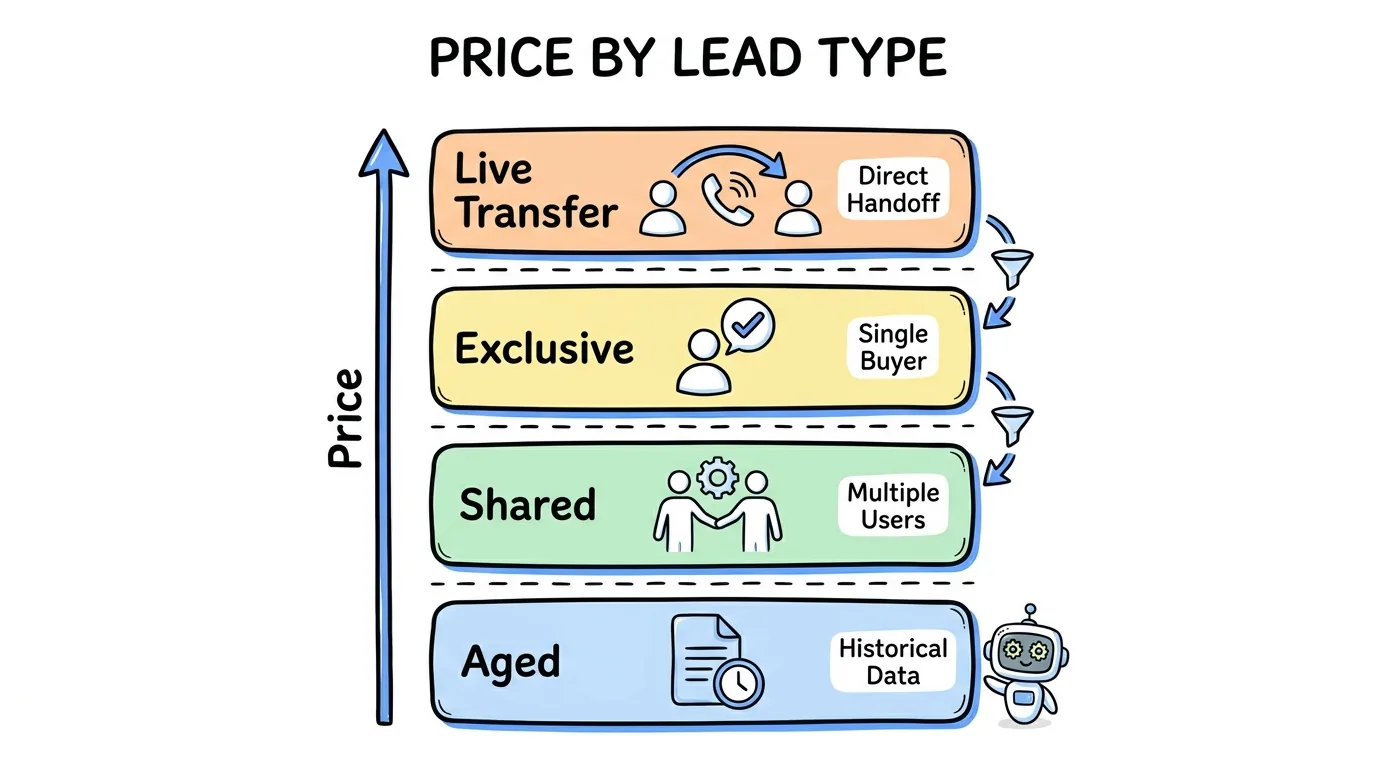

Types of Auto Insurance Leads

Not every auto record is worth the same, and pricing follows the type far more than the channel it came from.

- Exclusive leads go to a single buyer. They cost the most because there is no competition on contact, and agents close them at much higher rates.

- Shared leads are sold to two to four buyers at once. They are cheaper, move faster, and convert lower because several agents contact the same consumer.

- Live transfers and inbound calls route a screened caller directly to an agent. These command the highest payout per record because the consumer is already on the phone.

- Aged auto insurance leads are records that did not bind on the first pass, then resold days or weeks later at a steep discount.

High-risk and aged auto insurance leads deserve their own filters: SR-22 records, lapsed-coverage drivers, and telematics or usage-based insurance shoppers behave differently and should route to buyers who actually want them. For a full breakdown of recycled records, see our guide to aged leads.

Auto Insurance Lead Pricing Benchmarks for 2026

The table below reflects typical 2026 market ranges observed across the Lead Distro AI network. Treat them as a starting floor; California, Texas, Florida, and Michigan run 20% to 40% higher because of premium size and carrier density.

| Lead Type | Cost Per Lead | Typical Contact / Close | Best For |

|---|---|---|---|

| Shared (real-time) | $4 to $12 | High contact, 2% to 6% close | Volume buyers, multi-carrier agents |

| Exclusive (real-time) | $12 to $30 | Lower contact, 8% to 15% close | Agents who follow up in minutes |

| Live transfer / inbound call | $25 to $55 | 20% to 35% close | Carriers that staff a live desk |

| Aged (7 to 30 days) | $0.25 to $3 | Low contact, requires re-consent | High-volume dialers, nurture funnels |

The price gap between a shared and an exclusive record is the whole game in auto insurance lead generation. A shared lead at $6 only pays off at scale, while an exclusive at $20 only pays off if an agent calls within minutes. Worked example: buy 100 shared records at $6 ($600), and at a 4% bind rate with a $180 average commission, that is roughly $720 in revenue, a thin margin that duplicate detection and accurate billing decide.

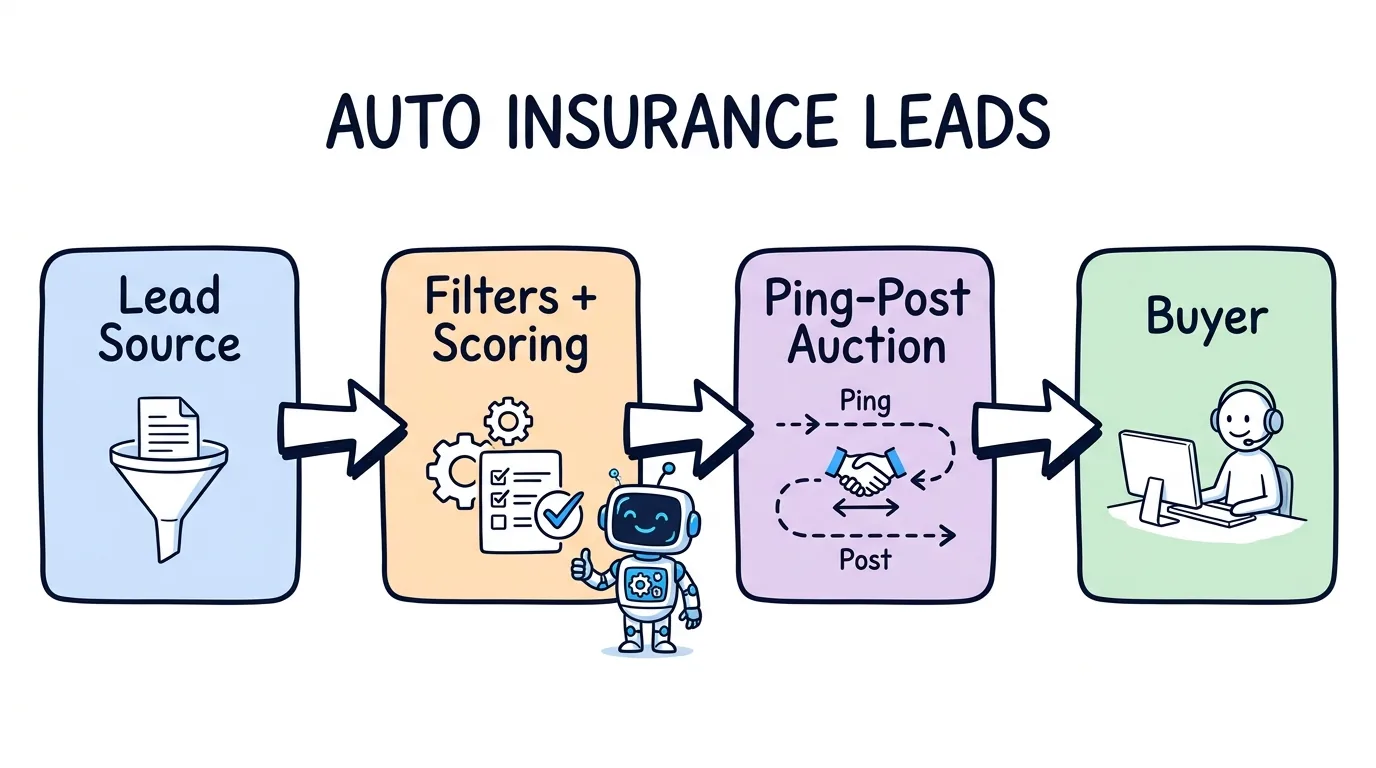

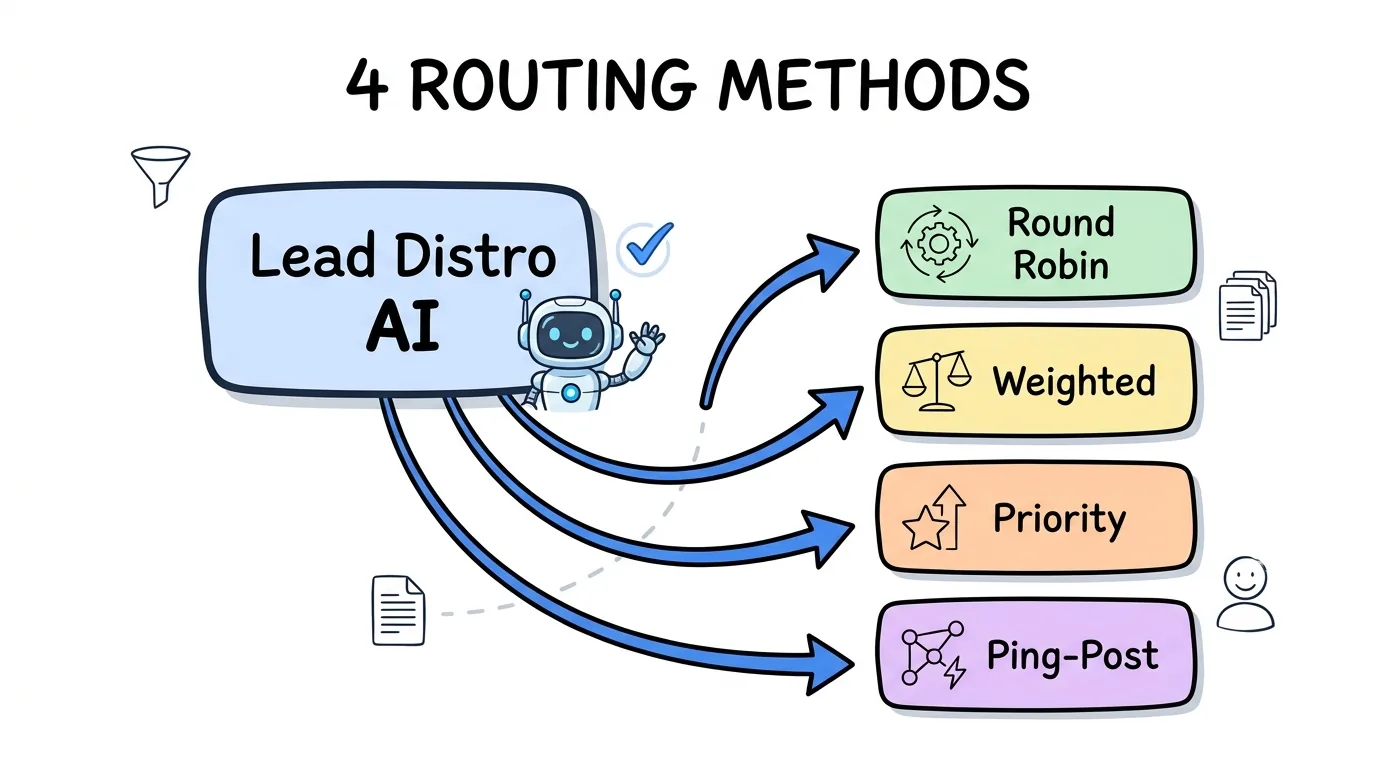

How Real-Time Auto Insurance Lead Distribution Works

Real-time auto insurance leads are delivered the instant a driver submits a quote form, and the delivery method decides how much revenue each record earns. The four core methods are Round Robin, Weighted, Priority/Waterfall, and Ping-Post.

Ping-post is the revenue maximizer. The platform first sends a partial record (ZIP code, vehicle, coverage, current-carrier flag, but no personal contact data) to multiple buyers, who bid in real time. The highest bid above your floor price wins, then the full record posts to that buyer by webhook or API. This real-time bidding turns every submission into an auction instead of a fixed-price sale.

Speed is the multiplier. Because Harvard Business Review research shows response inside an hour makes qualifying a lead nearly 7 times more likely, sub-second routing of real-time auto insurance leads directly lifts bind rates. You can see how lead distribution works end to end, or read how we handle insurance lead distribution across sub-verticals.

Filtering, Caps, and Compliance for Auto Insurance Leads

Clean routing is what separates a profitable book from a refund magnet. Set lead filters on state, ZIP code, driver age, SR-22 status, and currently-insured flags so a record only reaches a buyer who can actually use it. Daily lead caps stop you from overselling a buyer who cannot work the volume, and a suppression list plus duplicate detection keep you from billing the same consumer twice.

Compliance is non-negotiable in auto. The Telephone Consumer Protection Act (TCPA) requires prior express written consent before autodialed or prerecorded calls and texts, and every number must be scrubbed against the National Do Not Call Registry before outreach. Note one important nuance many guides get wrong: the FCC's one-to-one consent rule was vacated by the Eleventh Circuit Court of Appeals in early 2025 before it took effect, so a single clear consent disclosure remains valid (FCC). Even so, capturing per-buyer consent with TrustedForm or Jornaya is the safest practice, and serious buyers increasingly demand it.

How to Distribute Auto Insurance Leads at Scale with Lead Distro AI

Lead Distro AI was built for exactly this workflow: ingest auto insurance leads from any source, score them, filter them, and route them to the right buyer in under a second. It scores every lead with AI before routing, runs all four distribution methods, and shows real-time P&L by source, campaign, and buyer so you see margin as it happens.

The platform also handles the unglamorous parts that quietly leak money: duplicate detection across any field combination, a full buyer portal with self-serve caps and a prepaid wallet, return-and-credit handling, and status post-back by webhook so conversions flow back automatically. It runs auto insurance lead generation data and pay-per-call traffic in one platform, which removes the second dashboard most agencies juggle.

Plans start at $299 per month, with a 7-day free trial that does require a credit card so you see real profitability before you commit. Compare tiers on the Lead Distro AI pricing page.

Comparison: Auto Insurance Lead Distribution Methods

| Method | Revenue Per Lead | Setup Complexity | Best For |

|---|---|---|---|

| Round Robin | Fixed price, equal split | Low | In-house agent pools |

| Weighted | Fixed price, by performance | Medium | Mixed-quality buyer pools |

| Priority/Waterfall | Fixed price, cascade | Medium | Preferred carrier plus spot market |

| Ping-Post | Market price, live auction | High | Multi-buyer networks chasing max revenue |

Ping-post earns the most per record but needs the most infrastructure, since every bid and post has to be logged for dispute resolution. For sellers with three or more active auto buyers, ping-post usually pays for itself within the first month. This vertical is part of a broader cluster: the same routing and pricing logic applies to life insurance leads and health insurance lead generation, so a platform that handles one handles all three.

FAQ

How much do auto insurance leads cost in 2026?

Auto insurance lead costs in 2026 typically run $4 to $12 for shared records, $12 to $30 for exclusive real-time records, and $25 to $55 for live-transfer calls. Aged lists sell for $0.25 to $3 per record depending on age. Prices climb 20% to 40% in high-premium states like California, Texas, Florida, and Michigan because policy values and carrier density are higher there. Driver profile also matters: clean records cost less to source than SR-22 or high-risk leads, which carry a smaller but more motivated buyer pool.

What is the difference between exclusive and shared auto insurance leads?

Exclusive auto insurance leads are sold to a single buyer, so there is no competition on contact and agents close them at 8% to 15%. Shared leads are sold to two to four buyers at once, cost less, and convert at 2% to 6% because several agents call the same consumer. Exclusives win when an agent can follow up within minutes; shared leads win for high-volume operations where the lower price offsets the lower close rate. Most agencies run a blend and let speed to lead decide which one pays off.

Are aged auto insurance leads worth buying?

Aged auto insurance leads can be profitable when priced correctly and worked with a dialer or nurture funnel. Because they are 7 to 30 days old and sold for $0.25 to $3, the math works at volume even with low contact rates. The catch is compliance: under TCPA and Do Not Call rules, consent and DNC status must be re-confirmed before outreach, since the original consent may have aged out. Route aged records to buyers who specifically want them, and keep a suppression list so you never recycle the same record into the same buyer twice.

How fast do auto insurance leads need to be delivered?

Real-time auto insurance leads should be delivered within one second of submission. Harvard Business Review research found that contacting a lead within an hour makes qualification nearly 7 times more likely than waiting longer, and in auto the window is even tighter because consumers request multiple quotes at once. Real-time ping-post and instant webhook or API delivery let the first agent reach the driver before competitors do. Sub-second routing is the single biggest lever on bind rate, which is why distribution speed beats almost every other optimization.

Do I need TCPA consent to call auto insurance leads?

Yes. The Telephone Consumer Protection Act requires prior express written consent before placing autodialed or prerecorded calls and texts to a consumer, and every number must be scrubbed against the National Do Not Call Registry first. The FCC's one-to-one consent rule was vacated by the Eleventh Circuit Court of Appeals in early 2025 before it took effect, so a single clear consent disclosure is still legally valid. Best practice is to capture and timestamp consent with TrustedForm or Jornaya and route only to buyers covered by that consent, because many auto buyers now require it.

Conclusion

Auto insurance leads reward operators who treat distribution as the profit engine, not an afterthought. The price you pay to source a record and the price a buyer pays to receive it are fixed by the market, so your margin is decided in the middle: how fast you deliver, how cleanly you filter, how well you dedupe, and how accurately you bill. Get those four right and a thin per-lead spread compounds into a real book of business.

Lead Distro AI brings all four together with AI scoring, four distribution methods, real-time P&L, and a full buyer portal in one platform. Start your free trial and route your first auto insurance lead at scale today.

Ready to turn every submission into an auction? Lead Distro AI runs real-time ping-post across your buyer pool with AI scoring and sub-second delivery. Start your 7-day free trial and distribute your first auto insurance lead today.

About the Author

Founder & CEO of Lead Distro AI & Great Marketing AI

UC Berkeley graduate and former software engineer at Microsoft. Rafael built Lead Distro AI after managing over $10M in ad spend for performance marketing agencies (pay-per-lead and pay-per-call), including running campaigns for Neil Patel. He combines deep software engineering expertise with hands-on performance marketing experience to build tools that help these agencies scale profitably.

About Lead Distro AI

Lead Distro AI: AI-Powered Lead Distribution & Call Tracking That Maximizes ROI

The modern platform for pay-per-lead and pay-per-call agencies. Route, score, and deliver leads with AI-powered automation and real-time P&L tracking. Built for performance marketing agencies and lead buyers across legal, insurance, mortgage, solar, and home services verticals.

4 Distribution Methods

Waterfall, Round Robin, Weighted, Ping-Post

Ping-Post Auctions

Real-time bidding with sub-second routing

Real-Time P&L Reporting

Track revenue, costs, and profit per campaign

Call Tracking

Assign tracking numbers, record calls, and attribute conversions

AI Lead Scoring

Score every lead before routing to maximize conversion

Partner Portal

Self-serve dashboard for buyers to track leads