Exclusive Insurance Leads: Costs and How to Buy Them

Exclusive insurance leads sell to one agent and cost 2x to 4x shared leads. See pricing by line, buyer and seller economics, and how routing enforces it.

Rafael Hernandez

Founder & CEO

Ex-Microsoft SWE · $10M+ PPL ad spend

I hope you enjoy reading this blog post. If you want to try Lead Distro AI for free, click here.

Author: Rafael Hernandez | Founder & CEO of Lead Distro AI

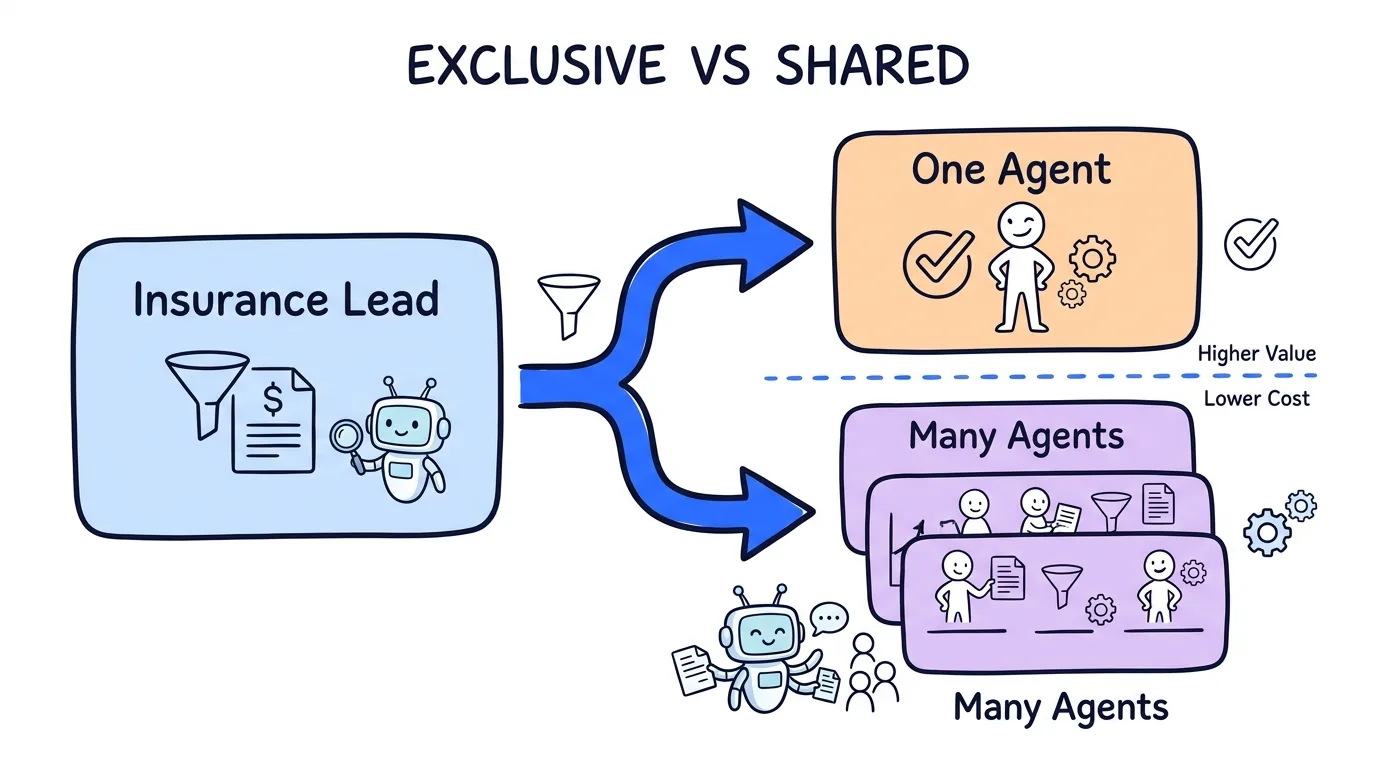

Exclusive insurance leads are policy shopper contacts sold to a single agent, so no competing agency calls the same prospect. They cost 2x to 4x more than shared insurance leads, which are sold to two to five buyers at once, but they convert at far higher rates because the buyer owns the entire follow-up. For most agents, the choice between exclusive and shared leads comes down to one trade-off: pay more per lead and win more of them, or pay less and compete on speed.

In short: Exclusive insurance leads maximize close rate and customer lifetime value. Shared leads maximize volume at a lower entry price. The line of business, your speed to lead, and your routing infrastructure decide which model returns more.

This guide breaks down what exclusive leads cost by line, the economics for both buyers and sellers, and how priority and waterfall routing actually enforces exclusivity so a lead is never double-sold by accident.

Key Takeaways

Exclusive insurance leadsare sold to one agent only and command a 2x to 4x price premium over shared leads in auto, home, life, health, and Medicare lines.Shared insurance leadscost less per contact but split the prospect across two to five buyers, so the winner is usually whoever calls first.- Speed to lead decides shared-lead outcomes. Contacting a web lead within five minutes versus thirty minutes changes qualification odds dramatically, per Harvard Business Review research.

- Sellers earn more per lead exclusively but more per campaign on shared. A blended model often beats committing to either extreme.

- Lead Distro AI enforces exclusivity with priority and waterfall routing, real-time duplicate suppression, and per-buyer caps so an exclusive lead is delivered to exactly one agent.

What Are Exclusive Insurance Leads?

An exclusive insurance lead is a person actively shopping for a policy whose contact information is delivered to exactly one agent or carrier. Because no other buyer receives that same prospect, the agent who purchases it owns 100% of the follow-up with zero competition on the phone.

That exclusivity is why agents pay a premium. When a Medicare broker buys an exclusive insurance lead during the Annual Enrollment Period, they know their intake team is the only one dialing that beneficiary. Compare that to shared leads, which insurers like Progressive, GEICO, and large independent agencies buy in bulk and race to call before four other call centers reach the same person first.

The trade-off for the buyer is cost. Exclusive auto, home, and life insurance leads routinely run two to four times the price of their shared equivalents. The trade-off pays off when your close rate and policy lifetime value justify the higher cost per acquisition, which is why high-value lines like final expense and Medicare Advantage lean exclusive.

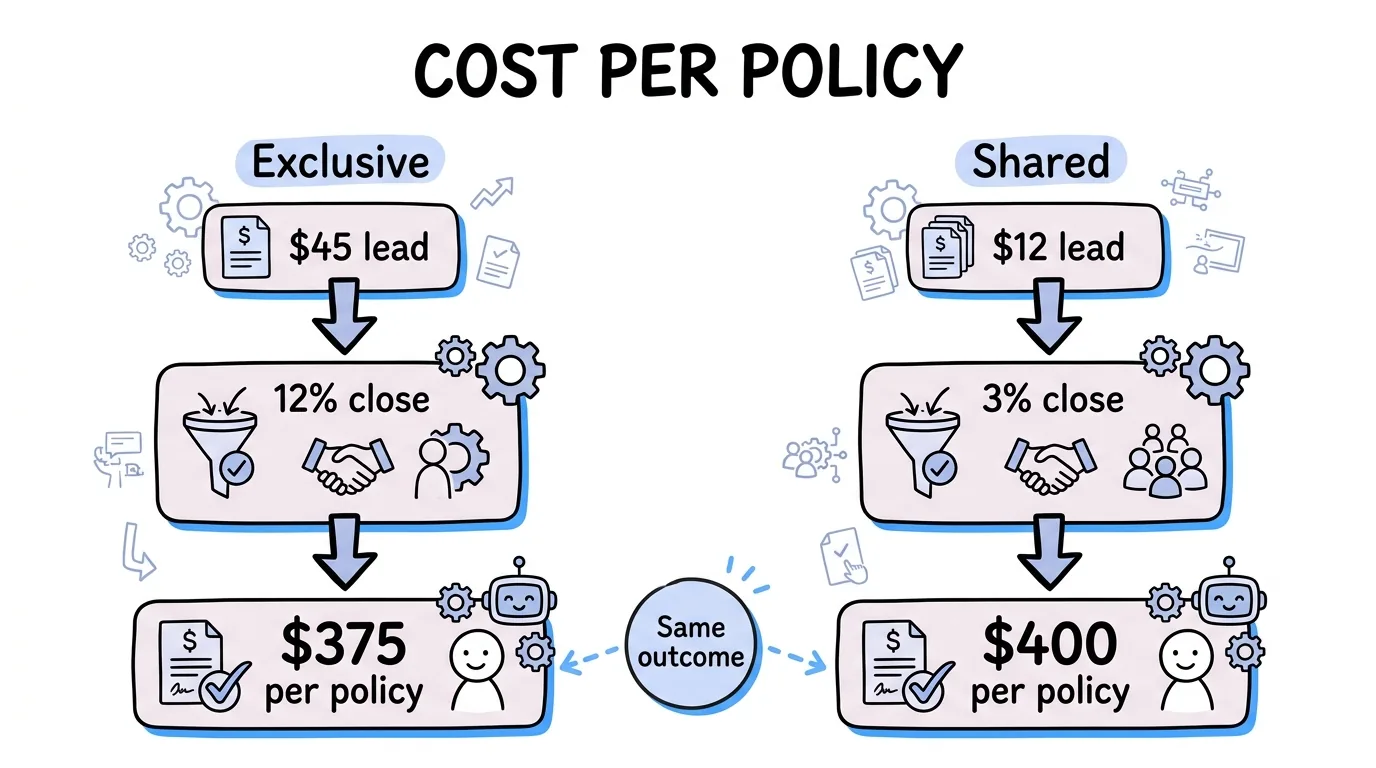

Exclusive vs Shared Insurance Leads: The Economics

The economics of exclusive versus shared leads are not about which is cheaper, but which produces a lower true cost per policy bound. A cheaper shared lead that closes at 3% can cost more per sale than an exclusive lead that closes at 12%.

Consider a worked example. An exclusive auto insurance lead at $45 that closes at 12% costs $375 per bound policy ($45 divided by 0.12). A shared auto lead at $12 that closes at 3% costs $400 per bound policy ($12 divided by 0.03). The "expensive" exclusive lead is actually the cheaper customer.

Shared leads still win in two scenarios: when your call center can dial within seconds and beat competitors on speed, and when buyer demand outstrips available exclusive volume. The Insurance Information Institute reports the average annual auto premium at well over $1,700, so even small close-rate gains compound across the policy lifetime. Run the math per line before you commit, and use the lead pricing calculator to model your own close rates against real costs.

What Exclusive Insurance Leads Cost by Line of Business

Exclusive insurance lead pricing varies widely by line because each line has a different policy value, sales cycle, and buyer competition level. The table below reflects typical real-time, in-market exclusive pricing in 2026, with shared prices shown for contrast.

| Insurance line | Exclusive lead price | Shared lead price | Why the gap |

|---|---|---|---|

| Auto insurance | $20 to $55 | $6 to $15 | High volume, fast renewal cycle |

| Home insurance | $25 to $60 | $8 to $18 | Often bundled with auto |

| Final expense / life | $30 to $90 | $10 to $25 | Long lifetime value, older buyers |

| Health / ACA | $15 to $45 | $5 to $14 | Open Enrollment demand spikes |

| Medicare Advantage | $35 to $100+ | $12 to $30 | Highest payout, CMS-regulated |

| Commercial / business | $40 to $150 | $15 to $45 | Complex, high-premium policies |

Medicare and final expense carry the steepest exclusive premiums because each bound policy is worth hundreds in commission over its lifetime, and the buyer pool of licensed agents is fierce during the Annual Enrollment Period. ACA and health leads surge during the Open Enrollment Period, when CMS reported record Marketplace enrollment of 21.4 million (CMS, 2024). When you decide to buy exclusive insurance leads, match the price you pay to the policy value of the line, not to a flat per-lead budget.

The Seller Side: Selling Exclusive vs Shared Insurance Leads

If you generate insurance leads to sell rather than to work yourself, the exclusive versus shared decision flips into a revenue-per-lead versus revenue-per-campaign question. Selling each lead once exclusively earns a premium price; selling it two to five times shared earns more total revenue from the same ad spend.

Here is the seller math. Generate a home insurance lead for $9 in Facebook ad spend, then sell it exclusively at $40 and you net $31. Sell that same lead to three buyers at $15 each and you collect $45 gross, netting $36, but only if all three deliveries succeed and return rates stay low. Shared selling wins on gross margin when buyer demand is deep; exclusive selling wins on buyer retention because exclusive buyers see higher close rates and stick around longer.

Most successful lead sellers run a blended model: route the freshest, highest-intent contacts as exclusive insurance leads to premium buyers, then sell the remainder as shared. For the full framework on rate-setting, see how to price leads by vertical and our pillar on exclusive vs shared leads.

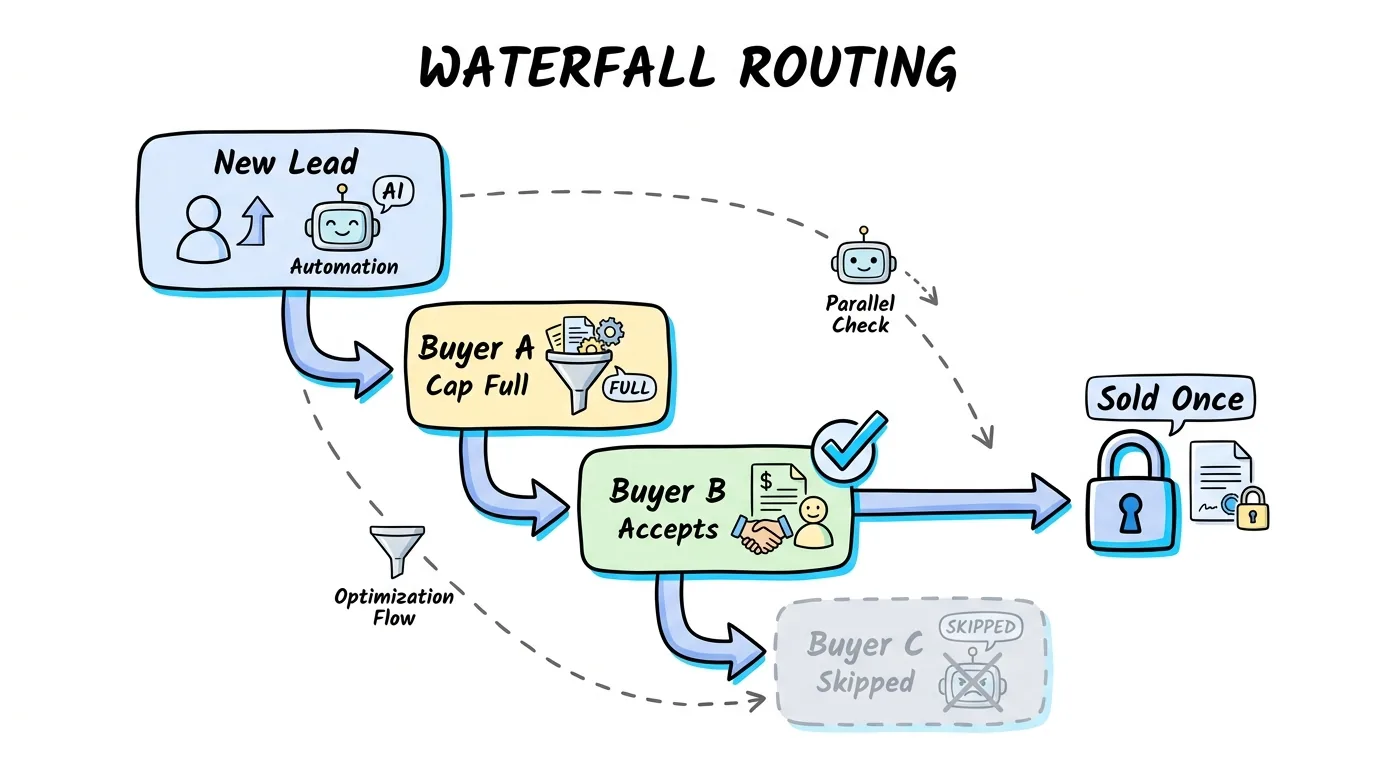

How Priority and Waterfall Routing Enforces Exclusivity

Exclusivity is a promise, and the only thing that keeps it is the distribution layer. If two buyers accidentally receive the same "exclusive" lead, you have a chargeback, an angry agent, and a damaged reputation. This is where routing rules do the real work.

Priority routing, also called waterfall distribution, offers each lead to buyers in a ranked order. Buyer A gets first refusal; if their daily cap is full or filters reject the lead, it cascades to Buyer B, then C, until one buyer accepts. The moment a buyer accepts an exclusive lead, the system marks it sold and removes it from every other queue. Combined with real-time duplicate detection and a suppression list, this guarantees one lead reaches exactly one buyer.

Lead Distro AI supports Round Robin, Weighted, Priority/Waterfall, and Ping-Post distribution, with per-buyer caps, geographic and license-state filters, and TrustedForm consent capture built in. To watch an exclusive lead route end to end, see how Lead Distro AI routes leads. For the broader vertical playbook, our insurance lead generation guide covers sourcing and compliance alongside distribution.

How to Buy Exclusive Insurance Leads Without Overpaying

Buying exclusive leads well is about verifying the exclusivity you are paying for, not just accepting a vendor's label. Ask three questions before you sign with any lead seller.

First, confirm delivery is real-time and the lead is suppressed from resale the instant you accept it. Second, demand TCPA documentation: the FCC sets penalties of $500 to $1,500 per violating call, so you need proof of prior express written consent, ideally a TrustedForm or Jornaya certificate. Third, test exclusivity by tracking how many of your "exclusive" prospects report being contacted by other agents; anything above a small fraction signals leakage.

"The agents who win with exclusive insurance leads are not the ones who pay the most, they are the ones who measure cost per bound policy and call within minutes," says Rafael Hernandez, Founder and CEO of Lead Distro AI. Speed matters even on exclusive leads. Harvard Business Review research found that firms contacting online leads within an hour were far more likely to qualify them than those who waited longer (HBR, 2011). When you are ready to test exclusive volume, start your 7-day Lead Distro AI trial and route your first batch with full exclusivity controls.

Frequently Asked Questions

What are exclusive insurance leads?

Exclusive insurance leads are policy shopper contacts delivered to one agent or carrier only, with no competing buyers receiving the same prospect. The purchasing agent owns 100% of the follow-up, which is why exclusive leads close at higher rates than shared leads. They typically cost 2x to 4x more per lead, but the lower competition and higher close rate often produce a lower true cost per bound policy in high-value lines like Medicare and final expense.

How much do exclusive insurance leads cost?

Exclusive insurance lead prices range from about $15 for ACA health leads to $100 or more for Medicare Advantage in 2026. Auto runs $20 to $55, home $25 to $60, and final expense $30 to $90. Shared versions of the same leads cost roughly one-third the price. Pricing tracks policy lifetime value: the higher the commission a line generates, the more buyers will pay for an exclusive, in-market prospect.

Are exclusive insurance leads better than shared leads?

Exclusive leads are better when your close rate and policy value justify the higher price and when you cannot reliably beat competitors on speed. Shared leads are better when your call center dials within seconds and buyer demand is high enough to keep volume flowing. Many agencies run a blended approach, buying exclusive leads for high-value lines and shared leads to fill pipeline volume at a lower cost.

How do I know my exclusive insurance leads are really exclusive?

Verify three things: real-time delivery with instant resale suppression, documented TCPA consent through a TrustedForm or Jornaya certificate, and a low rate of prospects reporting calls from other agents. A reputable seller uses duplicate detection and a suppression list so a lead is marked sold the instant one buyer accepts it. If prospects routinely say competitors called them, the "exclusive" label is not being enforced at the distribution layer.

Can I sell both exclusive and shared insurance leads?

Yes, and most profitable lead sellers do. A blended model routes the freshest, highest-intent contacts as exclusive leads to premium buyers, then sells remaining volume as shared to maximize total revenue per lead generated. Distribution software with priority routing and per-buyer caps lets you run both models from one feed, automatically enforcing exclusivity where you promised it while still monetizing shared volume.

Conclusion

Exclusive insurance leads are the higher-cost, higher-conversion path: one agent, no competition, and a true cost per policy that often beats cheaper shared leads once you do the math. Shared leads remain the volume play for fast-dialing call centers. Whether you buy them, sell them, or both, the difference between a profitable insurance lead program and a leaky one is the distribution layer that enforces exclusivity, suppresses duplicates, and routes every lead in real time. Get the routing right first, then scale the model that returns the most per policy bound, before a faster competitor claims the prospects you are paying for.

About the Author

Founder & CEO of Lead Distro AI & Great Marketing AI

UC Berkeley graduate and former software engineer at Microsoft. Rafael built Lead Distro AI after managing over $10M in ad spend for performance marketing agencies (pay-per-lead and pay-per-call), including running campaigns for Neil Patel. He combines deep software engineering expertise with hands-on performance marketing experience to build tools that help these agencies scale profitably.

About Lead Distro AI

Lead Distro AI: AI-Powered Lead Distribution & Call Tracking That Maximizes ROI

The modern platform for pay-per-lead and pay-per-call agencies. Route, score, and deliver leads with AI-powered automation and real-time P&L tracking. Built for performance marketing agencies and lead buyers across legal, insurance, mortgage, solar, and home services verticals.

4 Distribution Methods

Waterfall, Round Robin, Weighted, Ping-Post

Ping-Post Auctions

Real-time bidding with sub-second routing

Real-Time P&L Reporting

Track revenue, costs, and profit per campaign

Call Tracking

Assign tracking numbers, record calls, and attribute conversions

AI Lead Scoring

Score every lead before routing to maximize conversion

Partner Portal

Self-serve dashboard for buyers to track leads